25-28 June

Russian Petroleum and Gas Congress

Moscow Centre

Congress website, Sponsored by Industry

Program in English.

Travel Information

Delegate check list

Epilogue:The feast

Attending the Congress is an iteration in the forward movement on understandings about Russian oil and gas.

Attending the Congress is an iteration in the forward movement on understandings about Russian oil and gas.

On display are the particular feelings Russian academic and some industry and government have toward changes in markets and potential pipeline developments.

For example:

For example:

Despite recognition of immense importance of shale gas extraction in the United States upon Russian industry taking place at this meeting…

[including official denials of its importance, as witnessed by anyone attending Vladimir Putin‘s response to Daniel Yergin‘s question about changes to industry at the plenary of the St. Petersburg Economic Forum only days previously, when the Russian President announced there is no shale gas revolution in the US but in fact a short lived environmental disaster taking place]

— one main play is the rough-shod feelings expressed by Russian industry at the hands of their consumers, the Europeans, for whom they feel betrayed after having invested in building pipelines to the West.

That is to say, efforts associated with infrastructure so meticulously built up and managed by Russian personnel to deliver gas to Western Europe are ignored by consumer efforts to import global gas and renew attempts to create spot markets. For Americans, of course, this sentiment would fall on deaf ears, given the pipelines themselves are depreciated over a 20-year period after which, they simply become cash cows.

It is as if there is a certain nostalgia over infrastructure and what constitutes investment in Russian industry is the actual material placement and not its economic value.

At any rate — these are raw notes below taken as the days were long.

6/25 — Day Three:

Gas Day

Plenary Session

Russia’s Gas Industry: Strategies and Prospects The Russian Far East and Eastern Siberia as a New Gas Hub: Developing Production, Processing and Supply of Gas to the Asia-Pacific Region

Co-chairs: Torstein Indrebø, Secretary General, IGU, and Alexey Mastepanov, Academician and Deputy Director, Institute of Oil and Gas Problems, Russian Academy of Sciences. Alexey provides introduction. Demographic change and in particular, scientific and technical progress have changed the gas growth agenda, to a shift toward surplus energy where consumer will select their own energy and provider and area of consumption.

Co-chairs: Torstein Indrebø, Secretary General, IGU, and Alexey Mastepanov, Academician and Deputy Director, Institute of Oil and Gas Problems, Russian Academy of Sciences. Alexey provides introduction. Demographic change and in particular, scientific and technical progress have changed the gas growth agenda, to a shift toward surplus energy where consumer will select their own energy and provider and area of consumption.

Totally different criteria come into play. With the tightening competition of the consumer energy prices will fall. These processes are not alien to energy, even after the shale revolution in the United States. Technical changes do not remain the same. “Stone age did not end because we ran out of stones” — hydrocarbon age will not end because we run out of oil, but other advances toward a non-hydrocarbon era. Hopefully these issues will be discussed, to make us revisit these issues.

Anatoliy Arabskiy, Deputy Chief Engineer for Research, Technology and Ecology, Gazprom. Dobycha Yamburg, Innovation technologies in gas production and their influence on environmental protection. We have planned a number of environmental measures. Sustainable development. Describing technical changes to gas development that enhance environmental importance. Highly technical discussion about subsurface water movement.

Anatoliy Arabskiy, Deputy Chief Engineer for Research, Technology and Ecology, Gazprom. Dobycha Yamburg, Innovation technologies in gas production and their influence on environmental protection. We have planned a number of environmental measures. Sustainable development. Describing technical changes to gas development that enhance environmental importance. Highly technical discussion about subsurface water movement.

Alexey responds: Mr. Arabskiy clearly demonstrated there is significant cost reductions in efficiency in gas technology.

Vladimir Pashkov, First Deputy Chairman of the Government of Irkutsk region. Development of the East Siberian petrochemical cluster. Improvement of efficiency of oil and gas recovery by new technologies. We are subsidizing economies of other countries through lack of efficiencies. Unfortunately, increase in prices are not directly linked to economic performance. We are introducing a number of measures to maximize development and revenues. The premise that significant oil and gas reserves exist heighten potential for production. Proper geologic conditions for accumulations, existing transportation systems, modern chemicals, human and scientific resources are in place in Irkutsk and other factors give optimism. We are developing an oil and gas cluster — a complex that would increase production. Developing Irkutsk gas for export purposes. Creating a wealth fund for investment technologies.

Vladimir Pashkov, First Deputy Chairman of the Government of Irkutsk region. Development of the East Siberian petrochemical cluster. Improvement of efficiency of oil and gas recovery by new technologies. We are subsidizing economies of other countries through lack of efficiencies. Unfortunately, increase in prices are not directly linked to economic performance. We are introducing a number of measures to maximize development and revenues. The premise that significant oil and gas reserves exist heighten potential for production. Proper geologic conditions for accumulations, existing transportation systems, modern chemicals, human and scientific resources are in place in Irkutsk and other factors give optimism. We are developing an oil and gas cluster — a complex that would increase production. Developing Irkutsk gas for export purposes. Creating a wealth fund for investment technologies.

Dmitriy Sokolov, Researcher, Asia Pacific Energy Research Centre/APERC. Japan APEC energy demand and supply outlook 2013 by APERC: the role of natural gas in energy balance of APEC economies for the period till 2035. We do forecasting of energy to 2035 in Asia. A few words about APEC, examine energy sector in 21 companies, 60 percent of global energy demand in Asia. We develop research and cooperative programs for sustainable energy, fully financed by Japanese government. We do annual statistics, overview, demand and supply outlook (every four years), research support for cooperative programs. Programs: Oil and gas security exercise (GOSE) held in STPB, April 2013. and LNG Producer-Consumer conference held in Japan last year.

Scenarios: Business as usual (“Assumes existing policy continues, including polices in process of implementation, legislation already approved”) Three alternative cases: High gas scenario; Alternative urban development scenario; Virtual clean car race.

Scenarios: Business as usual (“Assumes existing policy continues, including polices in process of implementation, legislation already approved”) Three alternative cases: High gas scenario; Alternative urban development scenario; Virtual clean car race.

Key results: reducing primary energy intensity by 2035 is feasible. Nuclear electricity production increases. Gas based generation rises by 10 percent in contrast to coal.

To support large scale natural gas from Russia: Education–policy makers cannot take action without the support of their stakeholders and constituents. A completely wide difference between Russian and Australia. Australia is totally open (2) Promote energy efficiency-provide information and set standards for buildings, appliances, and vehicles, eliminate wasteful fossil fuel subsidies provide financing for cost-justified EE investments, promote Energy service companies (3) Promote energy research.

Anatoliy Panferov, Deputy Chairman of the Committee for Environmental Management, Ministry for Development of the Russian Far East of the Russian Federation. Formation and development of the Far East petrochemical cluster.

Anatoliy Panferov, Deputy Chairman of the Committee for Environmental Management, Ministry for Development of the Russian Far East of the Russian Federation. Formation and development of the Far East petrochemical cluster.

Samuel Lussac, Analyst, Wood Mackenzie, Vladivostok-LNG: promoting development of East Siberian gas. Vladivostok program. Both Russia government and Gazprom want to develop huge gas resources in Far East and market them in Asia.

How to Monetize East Siberian Gas reserves: Looking to supply China and Far East. Different supply zones using different scenarios of transport (pipe, LNG). All deposits located away from infrastructure, specific gas itself requires refining terminal. 30 to 40 billion dollar pipelines. As a consequence high capital costs makes projects marginal. Take away: Chayanda project not economic. Vladivostok market is not large enough to develop these fields. Joint development of Chayanda and Kovykta may be economic, if gas went to China and Vladisvostok. Mineral tax terms provided by Russian government are relaxed to stimulate pipeline projects. Unlocking Siberian gas would be very capital intensive and partners should be welcomed. Also, government tax regimes would be welcomed. Gazprom would have to capture the market there and competitive against other

Vyacheslav Kulagin, Head of the Global Energy Markets Centre, Energy Research Institute, Russian Academy of Sciences, Development prospects for the global gas market: new opportunities and risks. Share of gas will increase from 20 to 25 percent. All forecasts are bullish, but there is some question as to whether gas demand in Europe won’t be replaced by other non-Russian supplies. Important coincidence: this graph shows a share of Russian export is falling. In principle we hope that demand will grow that our deliveries will increase and that pipeline shipments will be supplemented by LNG but the competition is pretty tough. If we sum up the projects being built and contemplated for European export, we talk about doubling capacity. Just 5 years ago we expected major increase in exports to Europe. 200 bcm per annum is an positive assessment.

Vyacheslav Kulagin, Head of the Global Energy Markets Centre, Energy Research Institute, Russian Academy of Sciences, Development prospects for the global gas market: new opportunities and risks. Share of gas will increase from 20 to 25 percent. All forecasts are bullish, but there is some question as to whether gas demand in Europe won’t be replaced by other non-Russian supplies. Important coincidence: this graph shows a share of Russian export is falling. In principle we hope that demand will grow that our deliveries will increase and that pipeline shipments will be supplemented by LNG but the competition is pretty tough. If we sum up the projects being built and contemplated for European export, we talk about doubling capacity. Just 5 years ago we expected major increase in exports to Europe. 200 bcm per annum is an positive assessment.

Nabucco project unlikely. Azerbaijan will not approve. America: the shift to natural gas as a transportation fuel. The issues of pricing is major.

Vladimir Timoshilov.

Vsevolod Cherepanov, Member of the Management Committee, Head of the Gas, Gas Condensate and Oil Production Department, Gazprom. Gas-condensate assets: current situation and prospects. No show.

Vladimir Kontorovich, Laboratory Chief, A.A. Trofimuk Institute of Petroleum Geology and Geophysics, Siberian Branch of the Russian Academy of Sciences. Strategy and prospects of Russian gas industry development. No show.

Plenary Session 2

Strategies to Strengthen a Leading Position in the Global Gas Market: Energy Diplomacy, Development of Transportation and Processing Projects, Marketing South Stream Pipeline – Europe’s Vital Project

Co-Chairs: Uwe Fip, Senior Vice President, Gas Supply East, E.ON Global Commodities SE, John Roberts, Energy Security Specialist, Platts

Torstein Indrebø, IGU. Main driver we see is air quality and public health, where the gas industry can provide competitive solutions. Huge differences in European, American, and Asian gas prices. Can disparities between oil and gas be continued. Finally, if we shall success in the gas industry and reach global age of gas, we need to create more trust for the gas industry, climate groups, students.

Sergey Balashov, Deputy Head of the International Business Department, Gazprom, Gazprom and sustainable development. Speaking ironically about environmental concerns, giving an example of the imagined protection of an imagined whale.

Valeriy Minlikayev, Gazprom. Specific reservoir details.

Uwe Fip, Senior Vice President, Gas Supply East, E.ON. Global Commodities SE Security of supply and growth of new market segments for natural gas. Short term trading with gas structure. E. ON. has restructured. Reform of the malfunctioning carbon market in Europe is leading to power generation primarily led by coal and oil. New LNG and pipeline projects (from Russia) provide security. Ensuring that Gas supply in Europe is secure into the future. New applications for natural gas in Europe, transport sector, real boom is to be expected when LNG is used for long-haul trucks.

Uwe Fip, Senior Vice President, Gas Supply East, E.ON. Global Commodities SE Security of supply and growth of new market segments for natural gas. Short term trading with gas structure. E. ON. has restructured. Reform of the malfunctioning carbon market in Europe is leading to power generation primarily led by coal and oil. New LNG and pipeline projects (from Russia) provide security. Ensuring that Gas supply in Europe is secure into the future. New applications for natural gas in Europe, transport sector, real boom is to be expected when LNG is used for long-haul trucks.

Oleg Aksyutin, Member of the Management Committee, Head of the Gas Transportation, Underground Storage and Utilization Department, Gazprom, Energy efficiency of Gazprom gas transport projects.

Vitaliy Yermakov, Director, Russian and Caspian Energy, IHS Cambridge Energy Research Associates / IHS CERA, Changes in Russia’s LNG strategy and “Go East” gas policy. From the oil side, we will see major increase in LNG segment. It will be a resource to meet demand globally. Our team of economists at Goldman Sachs are saying that Asian countries are already outpacing Europe. By 2030 it will be growth of 7-8 percent. In 20 years Asia Pacific region, they will outpace Europe and America so dramatically, the west will not be able to catch up. “A new gas map of the world”.

Vitaliy Yermakov, Director, Russian and Caspian Energy, IHS Cambridge Energy Research Associates / IHS CERA, Changes in Russia’s LNG strategy and “Go East” gas policy. From the oil side, we will see major increase in LNG segment. It will be a resource to meet demand globally. Our team of economists at Goldman Sachs are saying that Asian countries are already outpacing Europe. By 2030 it will be growth of 7-8 percent. In 20 years Asia Pacific region, they will outpace Europe and America so dramatically, the west will not be able to catch up. “A new gas map of the world”.

New suppliers, with huge reserves. Traditional suppliers still here, won’t go away.

Shale gas put America at the top of the list. Turkmenistan will make an announcement soon which is huge. Traditional model suggested several major players with large reserves. In this tradition, huge pipelines would create supply to demand centers. But in the early 2000s with LNG, and now with new resources, are shifting this model.

In the US, everyone expected the States would become an importer, and created LNG terminals, and now, it is expected on being an exporter. The future is to what extent the US can be shifted to other parts of the world. Deepwater areas, huge reserves were discovered. From this perspective maintaining competitive costs. For Russia, the idea is to maintain competitive costs, or lower costs. We don’t expect major growth in the domestic market (Russia) so all expansion is largely for Asia.

Leonid Chugunov, Head of the Project Management Department, Gazprom “South Stream”: challenges and innovations. No show.

Ksenia Gladkova, Senior Adviser to the Secretary General, IGU Role of gas in global energy policies. I’m pleased to return to Moscow after presenting at the same conference. African members are displaying interest in joining us. Meeting in Azerbaijan, later this year in November.

John Roberts, last word — we had a strong stress on green house gas emissions, and ability of gas to mitigate issues. But we need to take a fresh look at the irony at the rise of CO2, that we live in an era of low coal prices and a lack of carbon prices that can mitigate. Four words: Supply is no problem. Security of supply is no problem and security of demand is the problem. Security of demand during G20 recently, took center stage, perfectly right, not because we’re here in Moscow, but because of the reciprocal nature of buying and selling. Politicization of security of supply and demand which impacts on long-term contracts, even though Norway was able to build the longest off-shore pipeline without any long term contracts, and it was the evident longterm supply that kept the market for that project moving forward.

John Roberts, last word — we had a strong stress on green house gas emissions, and ability of gas to mitigate issues. But we need to take a fresh look at the irony at the rise of CO2, that we live in an era of low coal prices and a lack of carbon prices that can mitigate. Four words: Supply is no problem. Security of supply is no problem and security of demand is the problem. Security of demand during G20 recently, took center stage, perfectly right, not because we’re here in Moscow, but because of the reciprocal nature of buying and selling. Politicization of security of supply and demand which impacts on long-term contracts, even though Norway was able to build the longest off-shore pipeline without any long term contracts, and it was the evident longterm supply that kept the market for that project moving forward.

“Politicization of Gas Corridors” — Role of government still important, I don’t know of any gas project that is not political. On the other hand, these political projects have to be commercial, you need two green lights. Just yesterday, in fact, there is not going to be a definable system (Nabucco) moving to Europe. Look around at Russia today, and you hear that phrase that Russia is an energy superpower, but you can also say the at the United States is an Energy Superpower, and the two are totally different species. They are the worlds two biggest developing hydrocarbon prospects.

Q & A: Game changers? [no one mentions bubble bursting in China] Remember that it was individual producers that provided innovation in shale, and it is doubtful that CNC or Rosneft or Gazprom, as large organizations can provide the kind of innovation that would be required to create a game changer.

Q & A: Game changers? [no one mentions bubble bursting in China] Remember that it was individual producers that provided innovation in shale, and it is doubtful that CNC or Rosneft or Gazprom, as large organizations can provide the kind of innovation that would be required to create a game changer.

6/25 — Day Two:

6/25 — Day Two:

Technical Session

Strategic Role of Drilling and Oilfield Services in the Development of Upstream Projects

Valeriy Bessel, Executive Vice President, NewTech Services; Professor, Gubkin Russian State University of Oil and Gas. The oil production paradox, or is it worth spending money on drilling. Main costs of vertical integrated companies is development costs. He notes there is more development activity in US than in Russia. “Drilling 5 times less, wellstock 5 times less, and well stock 3.5 times less, and yet we produce more than the United States. Maybe we do not need development drilling, or maybe the United States is wasting their time, because they don’t know where to to put it. My provocation speech, which I will answer at the end of the day”.

“Music in the hall is sponsored by Spacik company”.

“Music in the hall is sponsored by Spacik company”.

Konstantin Gribanov, Head of the Business Development Office, Rimera, Rimera’s Integrated approach to well service with guaranteed MTBF increases. Providing a service complex, with specially made metal technical products, leading to increased oil production and cost decreases.

Gavin Graham, Executive Vice President, Integrated Energy Services, Petrofac, New options for old fields: the changing role of oilfield service companies in extending the life of mature fields. West Siberia and Arctic possibilities for new development. 2064 oil reservoirs discovered, 1097 in production within 10 years.

Gavin Graham, Executive Vice President, Integrated Energy Services, Petrofac, New options for old fields: the changing role of oilfield service companies in extending the life of mature fields. West Siberia and Arctic possibilities for new development. 2064 oil reservoirs discovered, 1097 in production within 10 years.

Andreas Rentzsch, Vice President Sales, Bentec, Bentec’s “New Generation” cluster slider. New development in cluster slider for the Russian Market.

Andrey Petrakov, Director of the Scientific EOR Centre, VNIIneft, Using associated gas to enhance oil recovery. 24 percent flared gas instead of reinjection volume of natural gas. We do not pay due attention to gas. We had a decree adopted assigning 95 percent for gas utilization. Flaring gas is ecologically detrimental (see graph for details). Economic consequences of flaring, up to $13 billion per year through flaring. Difficult to stimulate subsurface developers to take advantage of associated petroleum gas (APG). Economic efficiency is not obvious.

Andrey Petrakov, Director of the Scientific EOR Centre, VNIIneft, Using associated gas to enhance oil recovery. 24 percent flared gas instead of reinjection volume of natural gas. We do not pay due attention to gas. We had a decree adopted assigning 95 percent for gas utilization. Flaring gas is ecologically detrimental (see graph for details). Economic consequences of flaring, up to $13 billion per year through flaring. Difficult to stimulate subsurface developers to take advantage of associated petroleum gas (APG). Economic efficiency is not obvious.

Valeriy Bessel returns to answer his question of why Russia bothers with oil development, given its inefficient comparison to the United States, and nevertheless increased capacity over US development. Well, “suggestion” — we have to drill or efficiently, but [?]

Plenary Session

Oil Exploration and Production in Russia: Trends and Prospects Oil and Gas Industry Innovation Development: Technological Instruments for Recovering Hard-to-Recover Reserves and EOR of Mature Fields

Oleg Pertsovskiy, R&D Director of the Energy Efficient Technologies Cluster, Skolkovo Foundation sponsors the plenary — first time participating in this conference, and starting the panel off. Viktor Martynov, Gubkin Russian State University of Oil and Gas, Introduces the panel.

Oleg Pertsovskiy, R&D Director of the Energy Efficient Technologies Cluster, Skolkovo Foundation sponsors the plenary — first time participating in this conference, and starting the panel off. Viktor Martynov, Gubkin Russian State University of Oil and Gas, Introduces the panel.

Gloom and doom over oil production in Russia. Our Ministry of Education, adopted governmental decree divided education into priority and non-priority. Where do you think oil and gas fell into? Non priority, even though 50 percent of industry of the country depends on this topic. First of all, it was a negative moral consequence for the industry, but even an economic decay, the difference of financing for this topic would be half lower. Also, it is impossible to train a theoretical person without practical training. I won’t dwell on it, but if you have a change, I would like to ask all of you, we have to speak up as oil men, oil and gas companies are writing letters to Ministry of Education, everyone is stating extreme things, such as Oil and Gas is not innovative or priority. So we’re going to discuss some technology issues, even though we won’t be able to develop the science. As [Joseph] Stalin said, “human resources are decisive for all”.

Gloom and doom over oil production in Russia. Our Ministry of Education, adopted governmental decree divided education into priority and non-priority. Where do you think oil and gas fell into? Non priority, even though 50 percent of industry of the country depends on this topic. First of all, it was a negative moral consequence for the industry, but even an economic decay, the difference of financing for this topic would be half lower. Also, it is impossible to train a theoretical person without practical training. I won’t dwell on it, but if you have a change, I would like to ask all of you, we have to speak up as oil men, oil and gas companies are writing letters to Ministry of Education, everyone is stating extreme things, such as Oil and Gas is not innovative or priority. So we’re going to discuss some technology issues, even though we won’t be able to develop the science. As [Joseph] Stalin said, “human resources are decisive for all”.

Oil could even be considered a renewable source, when such fields like Remashkena, we produce more oil than appraised, that perhaps oil is not created at the same speed as we learned it, the problem is that there is no science on the topic and it needs to be explored, unless we miss another revolution — if we find out [for example] if field reservoir production is different that we understand [to allow oil to accumulate], just an example of the great discovery and changes that we are going to face. It is essential to understand our position, in order to have functions achieved special for this country, not just for oilers but for general public, every scholar and economist will see that every one job in the oil sector creates 12 jobs elsewhere.

Oil could even be considered a renewable source, when such fields like Remashkena, we produce more oil than appraised, that perhaps oil is not created at the same speed as we learned it, the problem is that there is no science on the topic and it needs to be explored, unless we miss another revolution — if we find out [for example] if field reservoir production is different that we understand [to allow oil to accumulate], just an example of the great discovery and changes that we are going to face. It is essential to understand our position, in order to have functions achieved special for this country, not just for oilers but for general public, every scholar and economist will see that every one job in the oil sector creates 12 jobs elsewhere.

Renat Muslimov, Board Member, Tatneft; Adviser to the President of the Republic of Tatarstan on the Development of Oil and Gas Fields. Russia needs to optimise oil recovery and maximise EOR. The status of oil industry as reproduction of reserves and oil recovery ratio. When we ignore everything, everything looks fine, but if we look at it scientifically we recognize some distinctions that we should not speculate and manipulate. Let’s do it as the Americans do it. No one will do without the oil syringe. Back in the Soviet time, the project was 580 million tons, but we have 640 million tons. We have to face the corruption. Easier to go along with payolla. The same with oil, we really have to proceed with the reality of demand. We are not reassuring reproduction. Couple of comments on Ramashka. The older systems seems to be much better than the latest system of realizing production. A complaint against the shift from technocratic authority over reproduction to bureaucratic and economic authority.

Dmitriy Kryanev, Academician, General director, VNIIneft. The current state and prospects of oil recovery from fields with hard-to-recover reserves. Begins with BPs annual 2011 chart of what is economic. Different methods for recovery (thermal, chemical) EOR methods. North Sea uses good recovery methods (CO2 sequestration). Shale gas in US is shifting to oil, because of drop in prices. Horizontal drilling and multi-scale fractioning. Data on US production of Shale, previous year 13 percent, maximum production 66 million tons by 2030. Average oil recovery in global, 30 percent, US 39 percent, Norwegian 50 percent. In Russia, official recovery rate is 38 percent.

Dmitriy Kryanev, Academician, General director, VNIIneft. The current state and prospects of oil recovery from fields with hard-to-recover reserves. Begins with BPs annual 2011 chart of what is economic. Different methods for recovery (thermal, chemical) EOR methods. North Sea uses good recovery methods (CO2 sequestration). Shale gas in US is shifting to oil, because of drop in prices. Horizontal drilling and multi-scale fractioning. Data on US production of Shale, previous year 13 percent, maximum production 66 million tons by 2030. Average oil recovery in global, 30 percent, US 39 percent, Norwegian 50 percent. In Russia, official recovery rate is 38 percent.

Oleg Pertsovskiy, R&D Director of the Energy Efficient Technologies Cluster, Skolkovo Foundation. The Skolkovo Foundation’s role in supporting innovative development of the oil and gas industry. Describing Skolkovo set up how and why. Mentioned today already that many conversations about resource reproduction as a priority sector. We cannot just switch from oil to something else, for example, internet technology. We have to make use the resource as best as possible, value added. If we look at different institutes, all oriented toward different projects. We are focused on moving from R&D to marketability. Talking now about the set up of Skolkovo. Over 1100 proposals were received, over 240 when through review, 40 projects received funding.

Oleg Pertsovskiy, R&D Director of the Energy Efficient Technologies Cluster, Skolkovo Foundation. The Skolkovo Foundation’s role in supporting innovative development of the oil and gas industry. Describing Skolkovo set up how and why. Mentioned today already that many conversations about resource reproduction as a priority sector. We cannot just switch from oil to something else, for example, internet technology. We have to make use the resource as best as possible, value added. If we look at different institutes, all oriented toward different projects. We are focused on moving from R&D to marketability. Talking now about the set up of Skolkovo. Over 1100 proposals were received, over 240 when through review, 40 projects received funding.

Alexander Sitnikov, Director of the Oil and Gas Field Development Department, GazpromNeft Scientific Research Centre. The main technological challenges of and potential for increasing the efficiency of oil field development. What are key challenges? Talking in very technical language. … Improving regulatory framework of Russian oil and gas industry.

Ilya Mandrik, Vice-President for Geological Exploration, LUKOIL. Developing innovative geological exploration technologies on Russian offshore fields. Talking about offshore Arctic, implementing technical and regulatory competence, building up.

Ilnur Shigapov, Manager for Development in Russia, TGT Oil and Gas Services. Complex oilfield research to optimise mature field development systems. Rather technical. The previous speaker suggested regulatory changes to enhance offshore developments, in the Arctic for example (which Bessel suggested that Russian industry in comparison to the US are, on offshore, in an infant stage of development). The slides are available on the left.

[Just as an aside, I had a fabulous conversation with a German Service Company provider, Larissa XXX, who described in some detail how tenders obtain contracts with oil companies, including the importance of networking and its relationships to quality]

Dmitry Khlebnikov, Molten Group. Tools to support innovative development of the industry. Ranking a company based on a model for innovation. Usually, Russian companies rely on the innovation on foreign companies. Foreign companies typically rely only 25 percent on outside the shop technologies. Innovative strategies are not the same for every industry. Obviously we can’t do everything by ourselves, and we should not. But to understand who and how we should rely, a few categories, significance of the technology to our company, etc, and if we judge ourselves based on this model (slides) we can know what we need. Technological independence, if we think about it, if we purchase ready made technology, we take on long-term risks. We have technological dependency from companies. We have to create innovation. Different institutions, partnerships, universities can be involved, venture, Skolkovo, implementation of technology. Despite the fact, here are a few examples of good examples of partnership.

Dmitry Khlebnikov, Molten Group. Tools to support innovative development of the industry. Ranking a company based on a model for innovation. Usually, Russian companies rely on the innovation on foreign companies. Foreign companies typically rely only 25 percent on outside the shop technologies. Innovative strategies are not the same for every industry. Obviously we can’t do everything by ourselves, and we should not. But to understand who and how we should rely, a few categories, significance of the technology to our company, etc, and if we judge ourselves based on this model (slides) we can know what we need. Technological independence, if we think about it, if we purchase ready made technology, we take on long-term risks. We have technological dependency from companies. We have to create innovation. Different institutions, partnerships, universities can be involved, venture, Skolkovo, implementation of technology. Despite the fact, here are a few examples of good examples of partnership.

We need to communicate using our R&D initiatives:

Viktor Baldin, Chief Geoscientist, GEOSTRA Prospects of oil and gas presence in Gydan and the western part of Taymyr. Mainly technical, suggesting possible reservoirs. Reserves and assessment, preliminary assessment suggests this area has a tremendous amount to reserves.

Viktor Baldin, Chief Geoscientist, GEOSTRA Prospects of oil and gas presence in Gydan and the western part of Taymyr. Mainly technical, suggesting possible reservoirs. Reserves and assessment, preliminary assessment suggests this area has a tremendous amount to reserves.

Done with the list of speakers with just a few minutes before lunch, as originally discussed, let’s have a few questions or remarks. First question. Remark regarding the Gubkin University. You mentioned that a memorandum has to be signed. Let’s do that. Okay dear colleagues, the question was, why all the R & D organizations and oil companies do not communicate with each other?

We just view ourselves as competitors instead of cooperation, placing bids, we are not very well used to partnerships in the context of competition. As of today, major oil companies have 30 years of fundamental sciences and exchanges with universities. We do not put a long term forecast beyond a few years, and in comparison to Western companies R&D, they have 20 times more, and we have not adequately funded science. So there is not government policy and incentivizing R&D, yes, as to short term, but not long term. Maybe Skolkovo would like to comment.

Yes. Well, maybe the cooperation may not be at the extent we want yet, but there are a quite a number of companies that are getting together, and there is increasing cooperation, and finding some common ground, yes indeed we have such ground for cooperation. Question: To what extent is Skolkovo prone to cooperation? We try to do our best to be a catalyst for this approach, whether we have done it correct or not, we are not the sole initiators of this process, whether it remains a bureaucratic move (sponsored by ministry) or otherwise, we are starting it.

6/25 — Day One:

Plenary Session One

Russia’s Oil and Gas Industry: Responsibly Energising a Growing World

Getting Started: Chair, Pierce Riemer, General Director, World Petroleum Council/WPC, thanking everyone and reiterating his pleasure to attend. Vladimir Evtushenkov, Chairman, Russian National Committee of the World Petroleum Council / RNC WPC. Chairman of the Board, Systema, now stating that this is the only Russian oil and gas Congress of its kind, and that there are unique challenges, to assess prospects of business developments, to be discussed at all levels, and on behalf of the Russian government, “I would like to greet everyone involved to have successful Congress. Thank you for your kind attention”.

Getting Started: Chair, Pierce Riemer, General Director, World Petroleum Council/WPC, thanking everyone and reiterating his pleasure to attend. Vladimir Evtushenkov, Chairman, Russian National Committee of the World Petroleum Council / RNC WPC. Chairman of the Board, Systema, now stating that this is the only Russian oil and gas Congress of its kind, and that there are unique challenges, to assess prospects of business developments, to be discussed at all levels, and on behalf of the Russian government, “I would like to greet everyone involved to have successful Congress. Thank you for your kind attention”.

Kirill Molodtsov, Deputy Minister, Ministry of Energy of the Russian Federation. An honor and privilege to greet you here. If I ever tried to describe what is going on with one word in oil and gas, that word is “change”.

Last week in St. Petersburg, at the Economic Forum, President Vladimir Putin described these changes, and all those changes are visualized by us right now, what are we going to do, making an agenda, keep up — what forms those new trends. So this topic is worthwhile to discuss in the framework of the Congress, and we will talk about how the market of hydrocarbon marketing are being constructed, global bench marks, and as Lewis Caroll, stated in Alice and Wonderland, we have to run and lead the motion, and with the launch of Siberian sources, we have to lead the changes, shipping and pricing indexes, the global context, how to measure it, count it, how to proceed from transactions, OTCs, coal, crude oil, gas. Let’s get down to work.

Last week in St. Petersburg, at the Economic Forum, President Vladimir Putin described these changes, and all those changes are visualized by us right now, what are we going to do, making an agenda, keep up — what forms those new trends. So this topic is worthwhile to discuss in the framework of the Congress, and we will talk about how the market of hydrocarbon marketing are being constructed, global bench marks, and as Lewis Caroll, stated in Alice and Wonderland, we have to run and lead the motion, and with the launch of Siberian sources, we have to lead the changes, shipping and pricing indexes, the global context, how to measure it, count it, how to proceed from transactions, OTCs, coal, crude oil, gas. Let’s get down to work.

Renato Bertani, President, World Petroleum Council / WPC. First of all I would like to thank everyone, and be very brief about the importance of Russia in the oil industry and global context. A few facts, looking back 150 years, fossil fuels, account for 80 almost 90 percent of energy consumed by the world. Looking forward over the next 40 years, all projections are that oil and gas will be the main sources of development for sustainability, 60 to 70 percent of global needs. Certainly in this context Russia is the most important sources of hydrocarbons, in addition to conventional sources, IEA assessed unconventional oil, Russia has the largest potential, 75 billion barrels of additional unconventional oil. The message is the next year here in Moscow, the 21st Petroleum Congress, giving Russia its importance in the global context.

Renato Bertani, President, World Petroleum Council / WPC. First of all I would like to thank everyone, and be very brief about the importance of Russia in the oil industry and global context. A few facts, looking back 150 years, fossil fuels, account for 80 almost 90 percent of energy consumed by the world. Looking forward over the next 40 years, all projections are that oil and gas will be the main sources of development for sustainability, 60 to 70 percent of global needs. Certainly in this context Russia is the most important sources of hydrocarbons, in addition to conventional sources, IEA assessed unconventional oil, Russia has the largest potential, 75 billion barrels of additional unconventional oil. The message is the next year here in Moscow, the 21st Petroleum Congress, giving Russia its importance in the global context.

Andrey Tretyakov, Acting CEO, Rusgeology. How to create funding, actively discussing public private partnerships, putting together algorithms for development of new territories.

Andrey Tretyakov, Acting CEO, Rusgeology. How to create funding, actively discussing public private partnerships, putting together algorithms for development of new territories.

Ivan Grachev, Chairman, State Duma Committee of Energy — you are expecting from me the brief address. I express my sincere respect. Common knowledge that half of our budget comes from petroleum. A private story, we argued with professionals what would be the pricing scenario, and there was quite a panic in government, and they tried to push through Duma a crisis package, channeling the surplus of money to bank accounts in the West.

Conservative accounts to about $90 per barrel. I chose $100 per barrel, why was I correct? My desire was trying to understand realistic trends, and I was sure there was not going to be a second wave of crisis, and it is my perception that current crisis theories are virtual theories, and that real and virtual indices are determining global forecasts, but we are entering into a new stage, and that there is no reason to believe we will be entering into a second phase of crisis, and I am absolutely skeptical about renewables and am 100 percent sure that oil and gas will keep rising, by what margin will be arguable, but these fundamental baseline ideas.

Allow me to make my judgement about markets. If we say that crises emerge at real and virtual worlds, there should be another financial bubble, and that the next global financial bubble will be shale gas and shale oil and gas. Absolutely utopia the idea that Germany will be self reliant on wind. If I come back to our Russian laws, our fundamental premise that oil and gas prices will grow, and that China will need huge amounts of net clean energy, these assumptions allow us that the huge costs of development of eastern fields are quite justified. Therefore, the Duma will make necessary changes to the law. One small detail, the existing system of predictions could hardly be said to be acceptable, the system needs a lot of changes based on fundamentals.

Allow me to make my judgement about markets. If we say that crises emerge at real and virtual worlds, there should be another financial bubble, and that the next global financial bubble will be shale gas and shale oil and gas. Absolutely utopia the idea that Germany will be self reliant on wind. If I come back to our Russian laws, our fundamental premise that oil and gas prices will grow, and that China will need huge amounts of net clean energy, these assumptions allow us that the huge costs of development of eastern fields are quite justified. Therefore, the Duma will make necessary changes to the law. One small detail, the existing system of predictions could hardly be said to be acceptable, the system needs a lot of changes based on fundamentals.

Valeriy Yazev, First Deputy Chairman, State Duma Committee of Natural Resources, Environmental Management and Ecology; President, Russian Gas Society, Natural gas and EU energy policy contradictions.

Thank you Mr. chairman. Forecasts to 2025. It is difficult to predict oil and gas markets, lacking are geopolitical considerations and internal politics. But OECD decides to restrict sources from non-OECD countries, difficult to determine. Changes, new refineries in Saudi Arabia, golden age of gas turns into renaissance of coal, and Europe forgets carbon free economy and embraces coal-based power plants, working in conjunction with wind, impacting our realities, we fail to use completely our fields in traditional production areas and push into Arctic offshore and eastern Siberia, and bust our budget.

Thank you Mr. chairman. Forecasts to 2025. It is difficult to predict oil and gas markets, lacking are geopolitical considerations and internal politics. But OECD decides to restrict sources from non-OECD countries, difficult to determine. Changes, new refineries in Saudi Arabia, golden age of gas turns into renaissance of coal, and Europe forgets carbon free economy and embraces coal-based power plants, working in conjunction with wind, impacting our realities, we fail to use completely our fields in traditional production areas and push into Arctic offshore and eastern Siberia, and bust our budget.

I don’t share Grachev’s assumption that we need to go into Arctic and bust our budgets, we have plenty of untapped oil and gas sources and non-conventional, a big impact on global environment, but fundamental strategies should be proved. Controversies in natural gas, energy dialogue. Early this year, there is a need to transform EU energy policy, and create modernization, and create new partnerships with Russia. In Europe, gas prices prove to be inefficient because of high costs, and that prices earlier to the crisis were better than now.

Renewables made a lot of progress by spending 100s of billions of Euros, and through subsidies, and imposing their regime on the markets. EU gives priority to renewable, but conventional which serves as reserves without subsidy is not reasonable in my opinion. European gas market is in ruins, and is the ideal storm. Before the 3rd energy package was approved in Brussels, I said “let’s stop arguing since it is approved, but let’s look where we are after 5 years [of high prices]”. But Russia makes long term investments for Europe for its long term benefit, and Europe turns around and does not want to repay this investment, and is responding to shale gas.

Our experts should be protected against such scenarios. What should be our interest in Europe, if it wants to impose spot prices, or competition?

Russia does not create oil prices and has indirect impact on gas prices. Long term contracts are an inherent aspect of oil contracts, and follows an ideal model, but should be linked to some market pricing mechanisms. At the end of the day, economic factors and consumers will determine the situation. Russia needs to be flexible, the controversies, the pace of our economy, 3.3 percent or whatever, but even at 4 percent, we are falling behind, in balance of exchange. The capacity of our domestic market, does not increase, making our manufacturing less competitive, and purchasing power of households falling, we should decrease the energy intensity of our economy.

Russia does not create oil prices and has indirect impact on gas prices. Long term contracts are an inherent aspect of oil contracts, and follows an ideal model, but should be linked to some market pricing mechanisms. At the end of the day, economic factors and consumers will determine the situation. Russia needs to be flexible, the controversies, the pace of our economy, 3.3 percent or whatever, but even at 4 percent, we are falling behind, in balance of exchange. The capacity of our domestic market, does not increase, making our manufacturing less competitive, and purchasing power of households falling, we should decrease the energy intensity of our economy.

Fernando Valenzuela, Ambassador, Head of European Union Delegation to Russia EU-Russia energy relations. A great pleasure for me to participate in this conference. Pleased to share with you some views on oil and gas markets. Oil and gas are primary in the EU economy. Anticipate oil imports by 90 percent by 2030. Energy markets are changing rapidly, as already mentioned. The recent rise of LNG and Shale gas revolution in United States, continues to have impact on Global gas. Commenting on suggested changes toward natural gas transportation. Having LNG refueling every 400 meters. In order to retain this market share, gas has to be competitive. US coal exports to Europe has risen to its highest level in 17 years. Coal prices having fallen 19 percent. Gas electricity plants unable to compete with cheap coal are shutting down. Russia should reflect on this situation and be more sensitive to these changes. Russia’s economy needs reform, the energy sector, the economy requires rationalization and modernization. Moreover, increasing efficiency can open up more resources for export. The basic relationship between EU and Russia needs reliability, and Russia, while needs compensation for its production, also needs to become more competitive working within a sound equal framework.

Leonid Bokhanovskiy, Secretary General, Gas Exporting Countries Forum/GECF. Natural gas developments in the context on the new energy map. Gas Exporting Countries Forum (GECF). Members and Observers. US will be a lead exporter, Offshore Africa is up and coming. Climate change regulation is moving to promote gas. On the other hand, the falling demand in Europe for natural gas because of the financial crisis is affecting gas developments. Shale gas is creating new opportunities and cautions. Increasing exports are destabilizing traditional contracts (EU), there is some unfeasibility about the longterm politics of development in the United States. In Europe, UK, and Poland, shale gas is under review. Uncertainties surrounding ultimate availability and the environmental impacts of energy production. The GECF represents the highest level of activities and vision. Second meeting will be in July 1 in Moscow.

Leonid Bokhanovskiy, Secretary General, Gas Exporting Countries Forum/GECF. Natural gas developments in the context on the new energy map. Gas Exporting Countries Forum (GECF). Members and Observers. US will be a lead exporter, Offshore Africa is up and coming. Climate change regulation is moving to promote gas. On the other hand, the falling demand in Europe for natural gas because of the financial crisis is affecting gas developments. Shale gas is creating new opportunities and cautions. Increasing exports are destabilizing traditional contracts (EU), there is some unfeasibility about the longterm politics of development in the United States. In Europe, UK, and Poland, shale gas is under review. Uncertainties surrounding ultimate availability and the environmental impacts of energy production. The GECF represents the highest level of activities and vision. Second meeting will be in July 1 in Moscow.

Vladimir Kornev, Executive Secretary of the 21st World Petroleum Congress; Director, Russian National Committee of the World Petroleum Council / RNC WPC, Russian National Committee of the World Petroleum Council: 55 years – results and prospects. Talking about the history of the WPC Council. From the very start, the Russian national committee was established by 14 legal entities. First and foremost, we represent the interests of our countries within the framework of the WPC, taking into account interests of other countries, realizing our activities promote the Russian oil and gas sector. Back in 1971, the Soviet Union hosted this conference (shows a video). Basically talking about the conference coming up and how anyone should participate. Let me remind you that we have a stand on the second floor, and we will celebrate the initiation of the congress with you.

Alexey Kontorovich, Member of the Russian Academy of Sciences, Chief Scientific Officer, A.A. Trofimuk Institute of Petroleum Geology and Geophysics, Siberian Branch of the Russian Academy of Sciences, The first decades of the 21st century – Russia’s role in world energy markets.

Alexey Kontorovich, Member of the Russian Academy of Sciences, Chief Scientific Officer, A.A. Trofimuk Institute of Petroleum Geology and Geophysics, Siberian Branch of the Russian Academy of Sciences, The first decades of the 21st century – Russia’s role in world energy markets.

Plenary Session Two

EXPERT DISCUSSION Strategic Alliances In the Global Oil and Gas Industry: Prospects and Challenges — The importance of strategic alliances for developing exploration and production projects and technology exchange ▪ International oil and gas projects with the involvement of Russian companies in Russia and abroad ▪ Transformation of the global hydrocarbon supply structure in the context of BRICS strengthening ▪ The role of international technology exchange in developing offshore fields

Moderator: Igor Vittel, Producer and Host, Observer TV Show, RBC TV, asking questions.

Experts:

Genadiy Shmal, President, Union of Oil and Gas Producers of Russia, gets a souvenir for being good at what he does. Turkey is involved in major projects, and any unrest will have some effect and will impact regional situations. Moreover, Turkey often acts on both sides, gives support to projects, but laying out alternative projects.

Experts:

Genadiy Shmal, President, Union of Oil and Gas Producers of Russia, gets a souvenir for being good at what he does. Turkey is involved in major projects, and any unrest will have some effect and will impact regional situations. Moreover, Turkey often acts on both sides, gives support to projects, but laying out alternative projects.

Anatoliy Dmitrievskiy, Member of the Russian Academy of Sciences, Director, Institute of Oil and Gas Problems, Russian Academy of Sciences, talking about the massive changes in shale, Gazprom lost 15 percent of its shale gas sales in Europe. I made presentation in Europe some years ago, and asking why Russia is allaying its pipelines to Europe when Europe is producing gas on its own. And in 1997, we began to suggest that we should be pushing East, but we should have done it earlier, that we should be shipping gas to China, while European price remains low. We’re used to the fact that Europe needs gas and we have gas, but Europe is becoming a buyers market, what will be oil and gas prices for gas, it would not be indexed to oil because gas prices are falling. We have difficult negotiations all the time.

Igor Vittel: We know for certain we are trading at a loss to us, as far as I understand. [Dmitrievskiy takes a phone call] Perhaps [Vladimir] Putin is calling you.

Igor Vittel: We know for certain we are trading at a loss to us, as far as I understand. [Dmitrievskiy takes a phone call] Perhaps [Vladimir] Putin is calling you.

Tatyana Mitrova, Head of the Oil and Gas Department, Energy Research Institute, Russian Academy of Sciences. All prices are created privately, the terms and conditions remain confidential, that the market is somehow creating some kind of natural economic price. You cannot expect to have a monopoly over an expected price. Aggressive pushes by Iraq, shale in US and decline of oil prices.

Vittel — If we look at the driver of global demand, China, if we look at the horror of the bubble that was supposed to create decline in oil prices, which is now about to explode, and we will see a rapid decline in oil prices and the Russian government will suffer.

Mitrova — Our economy is sensitive to slight changes in oil markets and from perspectives. The costs in Russia are 2 to 3 times higher than are competitors.

Vittel — Now Shale revolution is a good thing for Europe, though it is bad for us, even though the European shale project failed in my opinion, the Japanese in depth drilling, to what extent, new technologies of production can reshape the energy market, while LNG intended for US from Qatar, and found its way to Europe, talking about Angola and Nigeria, certainly intended to cut off China from encroachment on resources.

Vittel — Now Shale revolution is a good thing for Europe, though it is bad for us, even though the European shale project failed in my opinion, the Japanese in depth drilling, to what extent, new technologies of production can reshape the energy market, while LNG intended for US from Qatar, and found its way to Europe, talking about Angola and Nigeria, certainly intended to cut off China from encroachment on resources.

Valeriy Bessel, Executive Vice President, NewTech Services; Professor, Gubkin Russian State University of Oil and Gas — There is not a single country in the world that does not suffer from a need for oil and gas, it is a buyer’s market, but shifts occur. All predictions, BP, about Shtokman gas should be going to United States, now US is exporting. Venezuela is 100 percent linked to United States through oil sales. I don’t understand why they are dividing there. Disintegration of Soviet Union, we actually disintegrated a very powerful country, and 2.6 dollars per barrel for Rosneft, back in the Soviet Union. Rosneft has partnership with ExxonMobil, and the Russian budget may not survive.

Vittel — You should be careful, we just had the president announce the transnational railroad [laughter]. [Pause] Chinese economy will have a rapid decline with implications. I fully agree with the bad implications of the disintegration of the superpower that we were.

Vitaliy Yermakov, Director, Russian and Caspian Energy, IHS Cambridge Energy Research Associates/IHS CERA.

Over the past two weeks, I’ve been hearing the same thing. China will sooner or later will go into rapid decline. I am somewhat taken aback by this forecast, and we have decline of the economy what does that mean for us, if we compare with GDP in China. Of course China is ahead of everyone, in 20 years time, they will be so ahead, no one will catch up. The growth of the population, requires economic growth, providing energy resources. All the consultancy companies testified to the economy is reshifting from traditional centers of growth. But the slow down of growth does not necessarily mean that energy growth will decline. They have a traditional approach to the market. They supply from long distances, lengthy pipelines. Exporting LNGs, it becomes quite obvious, that possibly to have LNG floating facilities, as a global model.

Vitaliy Yermakov, Director, Russian and Caspian Energy, IHS Cambridge Energy Research Associates/IHS CERA.

Over the past two weeks, I’ve been hearing the same thing. China will sooner or later will go into rapid decline. I am somewhat taken aback by this forecast, and we have decline of the economy what does that mean for us, if we compare with GDP in China. Of course China is ahead of everyone, in 20 years time, they will be so ahead, no one will catch up. The growth of the population, requires economic growth, providing energy resources. All the consultancy companies testified to the economy is reshifting from traditional centers of growth. But the slow down of growth does not necessarily mean that energy growth will decline. They have a traditional approach to the market. They supply from long distances, lengthy pipelines. Exporting LNGs, it becomes quite obvious, that possibly to have LNG floating facilities, as a global model.

Vittel — Everything is against us. Will the government recognize the problem and embark on some interesting decisions [will some decisions take place]. Irina?

Vittel — Everything is against us. Will the government recognize the problem and embark on some interesting decisions [will some decisions take place]. Irina?

Irina Esipova, General Director, Centre for Communication Development in the Energy Sector. Well, in St. Petersburg, Mr. Putin announced that we need some kind of one stop shop center of energy communication. But the Chinese tend to say that every Chinese citizen eats one brick stone within one year period. They are advancing technologically, and penetrate into the Russian European market. Of course we have to face this challenge with courage and if we speak about the influence of the reputation of this country, the ITC, it is all very complicated, the only company active abroad and positively perceived, is the Lukoil company.

Valeriy Yazev, First Deputy Chairman, State Duma Committee of Natural Resources, Environmental Management and Ecology; President, Russian Gas Society.

Break outpanel: Communication Forum

Influence of the Reputation of Russian Oil and Gas Companies on Russia’s Position in the World

[An unusual panel. Last week in SPB Economic Forum, there was discussion on “perception” of Russia boards of directors. In this panel, perception of Russian energy companies was the main topic, ed.]

Panel chair, Irina Esipova, General Director, Centre for Communication Development in the Energy Sector, begins with a “positive surprise”. We have Konstantine [?] who receives an award as best journalist, correspondent for energy world energy journalism. Now, modern technologies not often used in our oil and gas companies. Only Lukoil is trying to enlarge its reputation in different companies, and has its emphasis on self representation.

Speakers: Natalia Grib, Head of the Analytical Centre, Gazprom Energoholding, speaking of Russia’s position in the international oil and gas market. Recently I see an increase in content in the media. Several years ago, we did not have a panel on how to present ideas, sometimes people would communicate. I think this is a huge step forward. Peculiarities of information flows in different territories that reflect oil and gas market trends. I have been writing 15 years with more than 3000 articles. My presentation to enlarge your views, if the journalists are here, they would not use my information, because it is open. How can we interpret information. Already the 13th year that it is losing its position, has now only a 3rd in the world.

Part of a huge global industry that influences Russian companies. These things are linked together but do not know how to use these tools from a PR point of view. I can recall yesterday, presenting forecasts up to 2025, only BP gives forecasts up to 2030, only in 5 years, there will be hardly anyone asks for the Lukoil forecast. In 2012 declined to 35%, BP experts say that coal is rising, energy of all developing on coal. The fundamentals of coal and gas is starting to rise into oil. Only 2 percent of renewables. If is for you to understand what we are living in and who we are working for.

Part of a huge global industry that influences Russian companies. These things are linked together but do not know how to use these tools from a PR point of view. I can recall yesterday, presenting forecasts up to 2025, only BP gives forecasts up to 2030, only in 5 years, there will be hardly anyone asks for the Lukoil forecast. In 2012 declined to 35%, BP experts say that coal is rising, energy of all developing on coal. The fundamentals of coal and gas is starting to rise into oil. Only 2 percent of renewables. If is for you to understand what we are living in and who we are working for.

Oil price was influenced by different factors. Sanctions against Iran, planned production declines in UK…. From speculative factors, so you as a company can influence the market, you can place news so that folks understand what is happening. US is trying to minimize imports, in Europe, there is slight decline, in China, you can see the increase of oil and gas imports.

If we try to enlarge analyze basis, include shale, condensate, etc. Russia is in first place in terms of all liquids. So it all means things are based on representation. Same information represented in different markets have different outcomes. USA will always reiterate their market is always doing well and imports are declining. During the last 5 years, they declined light oil fractions, but increased heavy oils, the import structure is being changed, they usually show that import of light is being declined, but when I hear the Russia decline, that Russia does not have enough of gas, this forecast is not true. Gas generation in Europe is in decline in favor of solar and gas, but it was not forecast, a scenario, that all forecast would not be correct, so what is the difference between forecast and professional speculation. Natural gas prices highest in East. US, power plants are built for the cheapest source, natural gas, in Europe it is built for coal and LNG. Situation in Europe reflected on major oil and gas companies.

If we try to enlarge analyze basis, include shale, condensate, etc. Russia is in first place in terms of all liquids. So it all means things are based on representation. Same information represented in different markets have different outcomes. USA will always reiterate their market is always doing well and imports are declining. During the last 5 years, they declined light oil fractions, but increased heavy oils, the import structure is being changed, they usually show that import of light is being declined, but when I hear the Russia decline, that Russia does not have enough of gas, this forecast is not true. Gas generation in Europe is in decline in favor of solar and gas, but it was not forecast, a scenario, that all forecast would not be correct, so what is the difference between forecast and professional speculation. Natural gas prices highest in East. US, power plants are built for the cheapest source, natural gas, in Europe it is built for coal and LNG. Situation in Europe reflected on major oil and gas companies.

Larisa Ruban, Director of the Dialogue Partnership East-West Centre, Energy Research Institution, Russian Academy of Science. Expert forecast for the energy sector of the Asia-Pacific Region and Russia’s place in this region. We performed an international surveys of professionals, decision makers, we asked from 16 countries in Eastern regions about consumption. China, India, both are big energy consumers and increasing. Experts provide their evaluation on demands of energy resources, and transportation and risks of conflicts and threats.

Larisa Ruban, Director of the Dialogue Partnership East-West Centre, Energy Research Institution, Russian Academy of Science. Expert forecast for the energy sector of the Asia-Pacific Region and Russia’s place in this region. We performed an international surveys of professionals, decision makers, we asked from 16 countries in Eastern regions about consumption. China, India, both are big energy consumers and increasing. Experts provide their evaluation on demands of energy resources, and transportation and risks of conflicts and threats.

When we talk about image, in the Pacific basin region, ranking countries based on leadership possibilities. No production without stability and safety. Only 13 percent of experts believe there is the possibility of world conflict. And over 70 percent believe it is low possibility. Image of Russia—What is the role of Russia in the far east, 46 percent says we have lost the position, behind the economic development in the region, even though in the past it held a higher position. Russia is a middle range player. But is increasingly changing its position and can work in the Far East, though skeptical. Chinese experts say they are stressing cooperation and not unions. They feel that Russia is very strong in oil and gas production, and the attitude is better toward Russia than USA.

Russia wants to play a leading role in Asia, but without the power to do so. Last year just 11 percent of experts felt Russia was a global power.

Yanina Dubeykovskaya, Co-Chairperson, Programme Director, “Communication on TOP” Communication Forum in Davos. Does energy need publicity? International experience. Came to Davos to organize energy. Of course we know that communication development is transparency and openness. The world is digitalized and outcomes of transparency cannot be predicted. The main measurement of efficiency of communication, and what influences our decisions. If our company is efficient and use of communication tools. First rule is competition. In China, internet is regulated by State and positioning of experts is totally different. Whether a company sees internet as a strategic tool, communication models based on b2b/b2c, private or publicity of the company and the first person in the company who is the main decision maker.

Yanina Dubeykovskaya, Co-Chairperson, Programme Director, “Communication on TOP” Communication Forum in Davos. Does energy need publicity? International experience. Came to Davos to organize energy. Of course we know that communication development is transparency and openness. The world is digitalized and outcomes of transparency cannot be predicted. The main measurement of efficiency of communication, and what influences our decisions. If our company is efficient and use of communication tools. First rule is competition. In China, internet is regulated by State and positioning of experts is totally different. Whether a company sees internet as a strategic tool, communication models based on b2b/b2c, private or publicity of the company and the first person in the company who is the main decision maker.

Systematic changes- even if we are not personally linked into internet digital, but more and more, the company’s image is influenced by the internet, communication is global and quick. If 10 years ago we needed to restrict information to a certain audience, today it is less and less our role, because it is impossible, we lose the reputational goals because it is impossible. From linear to cloud communication. If you do not have twitter, you will have a problem. Probably there can appear a person, the person starts influencing… local audiences.

Information is changed to a social phenomena. Not a simple logical structure, we need to involve people so that they share your values, we don’t inform any more, but involving people. Packaging of the content, a story, with a plot, a hero takes place of the abstract company, and you know that a lot of companies give a public face. Presenting the image of the company. All this data is influencing the fund market and creating reputations and this is the companies evaluation. The question is whether the companies image can create a positive image in investment society, create credibility. In energy sphere it is less presented, whether it can be applied to the energy sphere. I am a transparency addict. Having worked in the energy sector, it can be up to your personal principle, but whether required by market. It is not everything that much to the energy sector, but even this conservative sphere, that energy companies use naming to transparency and this new challenges presented markets information policy. Should be quicker should be wider, and we are for anti-crisis communication. If we need to always talk minister of emergency and understand the tools. The whole of the reputation is not only the company. The concept of reputation that haven’t even thought about. World energy brands. Internet channels. Lukoil, that is presented in digital channels. New trend of energy company, I could not find it. A few good on line channels, you tube, presentation of first persons in the company, Gazprom project that has 20 thousand viewers, a good thing about internet, it calculates statistics. We can see site traffic it is a good measurement of involvement.

Information is changed to a social phenomena. Not a simple logical structure, we need to involve people so that they share your values, we don’t inform any more, but involving people. Packaging of the content, a story, with a plot, a hero takes place of the abstract company, and you know that a lot of companies give a public face. Presenting the image of the company. All this data is influencing the fund market and creating reputations and this is the companies evaluation. The question is whether the companies image can create a positive image in investment society, create credibility. In energy sphere it is less presented, whether it can be applied to the energy sphere. I am a transparency addict. Having worked in the energy sector, it can be up to your personal principle, but whether required by market. It is not everything that much to the energy sector, but even this conservative sphere, that energy companies use naming to transparency and this new challenges presented markets information policy. Should be quicker should be wider, and we are for anti-crisis communication. If we need to always talk minister of emergency and understand the tools. The whole of the reputation is not only the company. The concept of reputation that haven’t even thought about. World energy brands. Internet channels. Lukoil, that is presented in digital channels. New trend of energy company, I could not find it. A few good on line channels, you tube, presentation of first persons in the company, Gazprom project that has 20 thousand viewers, a good thing about internet, it calculates statistics. We can see site traffic it is a good measurement of involvement.

Energy industry in general, is still very closed, when something happens, a crisis, there is a lot of unstructured information in media, and that is the specificity of the industry, if it is conservative, and should correspond to the changes of industry.

The image of the person should represent the main person of the company, they inform this or that about the company, the spokesperson places them into the spot light. And the person who has this function of the evangelist should have a talent of the digital auditorium.

Irina jumps in: Top managers do not represent the new understandings of the current situations. We provide a new forum to create a new set of understandings.

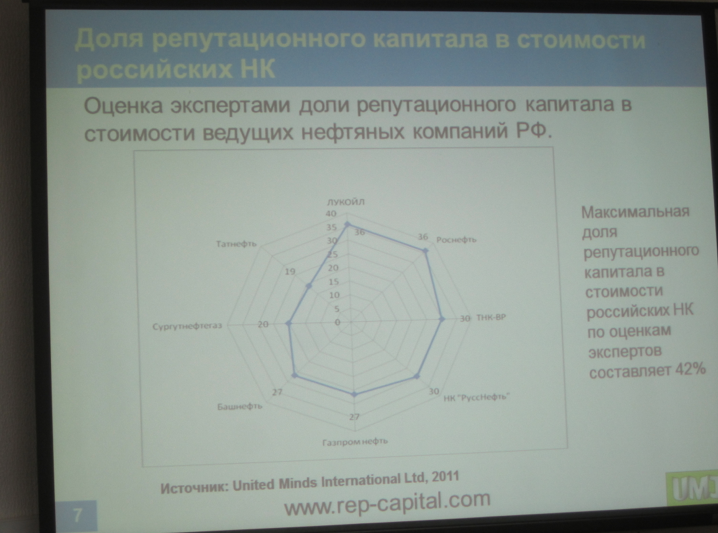

Alexey Fisun, Head of Reputation Research, United Minds International. The reputation capacity of Russian oil and gas companies – The topics of oil and gas are gendered, now I’m studying the male aspect of the corporate image, doing this now for several years. Analysis of expert opinion. I developed a system of reputational capital and present results related to energy industry. Why do you think Russian companies are interested in their reputations. In general. Crisis, catastrophe or if they have enough spare money. When the companies are going to place their assets on the public stock. Reputation when we need to attract investments. Different reputation than Dosteovesky or Pushkin. Reputation becomes material, and we need to assess the efficiency of PR services, or when PR is working really bad. We evaluate different industries – general assessment of industries, leading 20 companies? But are you from analytical sectors, when you have to deal with your reputation.

Alexey Fisun, Head of Reputation Research, United Minds International. The reputation capacity of Russian oil and gas companies – The topics of oil and gas are gendered, now I’m studying the male aspect of the corporate image, doing this now for several years. Analysis of expert opinion. I developed a system of reputational capital and present results related to energy industry. Why do you think Russian companies are interested in their reputations. In general. Crisis, catastrophe or if they have enough spare money. When the companies are going to place their assets on the public stock. Reputation when we need to attract investments. Different reputation than Dosteovesky or Pushkin. Reputation becomes material, and we need to assess the efficiency of PR services, or when PR is working really bad. We evaluate different industries – general assessment of industries, leading 20 companies? But are you from analytical sectors, when you have to deal with your reputation.

Index of reputation. Energy would be more than 5, the reputation of the business is not really high. Among this rather low evaluation, the energy complex, only gives way to high tech. (www.rep-capital.com).

What industries are more immune to crisis. Fuels are a little higher, (railways are more reliable than oil).

Answers of the experts

(1) bases of resources (2) connections with authorities. (3) Etc. look at slide (9) transparency of company…

Where in this list of the image of the company and reputation of the company. We are talking about what is related to reputation, everything is related to reputation. But nothing is related to reputation. Reputation in energetic company is not included. But what is a supplement for reputation for Oil Company – “Administrative Resources” no. 2 and no. 1 (being capable of stating factually what the company has in the ground).

Where in this list of the image of the company and reputation of the company. We are talking about what is related to reputation, everything is related to reputation. But nothing is related to reputation. Reputation in energetic company is not included. But what is a supplement for reputation for Oil Company – “Administrative Resources” no. 2 and no. 1 (being capable of stating factually what the company has in the ground).

We keep asking: financial factors. Business strategy, ethics of business, ethics of business (7th position). Corporate responsibility on the last place. There is a slide there that looks like a spider web. And this is about reputation. Connection of reputation of a company with shareholder expectation. General evaluation comes up to 42 percent.

Russian Company reputation. Somehow the scene in which they float is impacting the quality of fish itself. So the main importance and evaluation – gives us a tool to think about (www.united-minds.ru).

Vladimir Bachishin, Professor, Slovak Law University; Partner, Bachishin & Tkach Consultancy, Slovakia. The perception of Russian oil and gas companies in the European media –Analyzing media space assessing Russian oil and gas companies. Content analysis. A lot of definitions. Talking about linking personalities to gas developments in different areas.

Vladimir Bachishin, Professor, Slovak Law University; Partner, Bachishin & Tkach Consultancy, Slovakia. The perception of Russian oil and gas companies in the European media –Analyzing media space assessing Russian oil and gas companies. Content analysis. A lot of definitions. Talking about linking personalities to gas developments in different areas.